Detail of a mural by Ojibwe artist Cedar Eve Peters, honouring her ancestors (Photo, Jody Freeman)

If you are unlucky enough to live in Bangladesh, Nepal, North West India, the Caribbean or US Gulf Coast states right now, you are probably knee-deep in that old platitude, “What goes up (warm moist air) must come down (torrential rain).” In Canada, on the other hand, you may have been lulled into believing that the laws of gravity do not apply. The universal principle seems to have been waived in favour of the Canadian variant, “What goes up (property prices), goes up. Bloomberg News, housed in New York City, begs to differ.

“As safe as houses,” says the adage. Most people believe it has to do with the solidity of bricks and mortar, but the phrase seems to have been coined as a marketing ploy shortly after the not dissimilar expression, “as safe as the Bank of England.” And “safe” means certain or secure, not physically solid. It was developed as a selling slogan for real estate after the railroad investment bubble burst in the early decades of the 19th century. (Bubbles have that unfortunate propensity, but are rarely recognized for what they are until they do in fact burst.) At that time, housing was not viewed as a profitable investment, but rather as a reliable way of holding one’s wealth that couldn’t easily be stolen.

Recessions can be expected at least once a decade, depressions twice a century. Recession is usually followed by periods of investor caution before new “sure-fire” areas of investment come along, and caution is again scattered to the wind.

Economic crises are nothing new. The infamous 17th-century black tulip and 18th-century South Sea bubbles are simply older versions of the 20th-century dot.com or 21st-century sub-prime mortgage boom – and bust. Tulipmania is the first extensively documented economic bubble, but they all follow a similar pattern. For those not familiar with that story, tulips were introduced to the Netherlands as an exotic rarity from Turkey in 1593. Thanks to skilful speculative promotion, by the time their bubble burst in 1637, a single black tulip bulb was worth more than a wealthy merchant’s house, and many merchants sold their houses to get their hands on them. So heavily invested was the Dutch economy that despite government intervention and commitment to support tulip bulb prices at 10% of their previous peak, the crash that followed flipped the Netherlands into a decades-long recession.

The South Sea bubble took the idea one step further. At least tulip traders had traded tulips. The South Sea Company, which never traded in the South Sea, cut out all pretence and sold mere promises. Based on the economically successfully Dutch East India Trading Company, which did trade products, particularly slaves, Britain’s South Sea Company simply traded debt. How modern! Its collapse in 1720 threw the British and many other economies into recession.

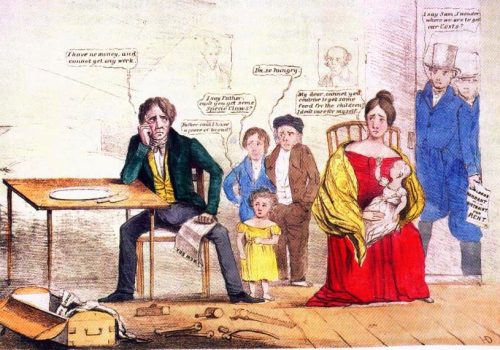

When share prices collapsed in the 1840s’ recession, many people lost a lot of money, even if it was money they had never seen and could not count physically. Historically, housing was rarely viewed as a great investment. As bookkeeping practices started to be standardized in the 19th century, it became easier to follow the rise and fall of markets. House ownership was viewed as a hedge against loss. Homes did not necessarily increase in value but owners did not lose, and people who owned enough of them were guaranteed steady incomes. From the 1840s on, house prices hardly rose, and following a worldwide recession towards the end of World War I, they fell. That recession was followed by the roaring twenties’ investment boom (read “bubble”) which most people now know led to the 1929 crash and the 1930s’ Great Depression. Property prices fell, not dramatically but enough to worry the wealthy, and only started to rise significantly during the 1950s. That rise reflected more than the upturn in the world economy. It was a tribute to successful marketing and to the ability of the movers and shakers of the world to build successful alliances.

In 1935 and 1936, legislation was introduced worldwide to regulate banking and the financial sector. Consumer banking was separated from investment banking, and insurance was decoupled from the banks. Measures aimed at preventing a repeat of the 1929 stock market crash were introduced. They largely succeeded. The financial sector was keen to fight them but needed to avoid attracting public opprobrium.

World War II provided great opportunities for people who had money to invest. The Bush family in the USA, for example, benefitted enormously, and had the McCarthy Committee (the House Un-American Activities Committee) not come along to persecute anyone who was not a friend of Senator McCarthy, George W. Bush’s grandfather would have faced war crime trials for having helped finance the Nazis in Germany. Instead, charges against Bush were dropped.

However, to the consternation of many involved in financial exploitation, from the wreckage of World War II arose an international community becoming incarnate in the United Nations. Through the Bretton Woods institutions, it spearheaded a financing system targeting the rebuilding and developing of the shattered world economy through international financial collaborative support for activities centred on economic growth. The World Bank and the IMF were born.

Their early development credentials were impeccable. Founders and many supporters genuinely saw them as enablers for countries struggling economically: those rebuilding after wartime destruction, and those striving to achieve their first economic advancement. For a couple of decades they did a great job, although they focused more on and succeeded in countries which were already economically developed. These two decades were put to good use by those who had other aims.

The bankers and financiers had new champions in Friedrich Hayek – the inspiration behind Milton Friedman and the Chicago School of Economics. In turn, Friedman provided a social and political model for politicians such as Augusto Pinochet, Ronald Reagan and Margaret Thatcher. Skilful political and media manipulation popularized Friedman’s views, ensuring that by the early 1980s, large enough numbers of believers in Friedman’s philosophy of monetarism were in position to ensure that policies based on his philosophy could be ushered in. Espousing the philosophy of Ayn Rand, which she called “the virtue of selfishness,” they managed to place Alan Greenspan, one of her cult followers (and they really were a cult), in a crucially influential position as the head of the US Federal Reserve.

Throughout the 50s and 60s, believers in monetarism were planted in universities, government administrations and political parties. Coalitions with right-wing media moguls were nurtured. Promoters of selfishness became significant opinion formers, blocking naysayers. Institutions were effectively taken over. One global group was essential to that process, and its takeover took a couple of decades. That institution, the closest we have ever come to a world government, was the United Nations Organization.

In its early days, opposing power blocs tried to co-opt the UN, but for years the idealism of some of its founders won out. Enlightened, progressive leaders like Sweden’s Dag Hammarskjold became Secretary General. His mysterious death in 1961 in a plane crash in Africa is worth studying, and an international commission of lawyers is currently doing that. But things changed with the appointment of a former Nazi, Austrian Kurt Waldheim, in 1972. Many UN veterans date the decline of UN morality back to his tenure, claiming that part of the change came about because of him selling favours. During his decade, more people came in whose motivations were driven by self-interest and greed, and the importance of exerting influence within the UN started to be recognized.

By the time Margaret Thatcher and Ronald Reagan headed their respective countries in the early 1980s, most of the elements were in place for a clean sweep. There is much talk nowadays of a revolving door between industry and government. Some examples include bankers doubling as civil servants to help ease banking regulations before returning to banking to reap the benefits, and accountants advising on major infrastructure projects before returning to private industry as consultants on those very projects. While companies have always lobbied governments, often in breach of explicit anti-lobbying legislation, the significance of the UN in formulating or encouraging international policy was not well recognized by major wielders of influence until the 1970s. So drug companies, for instance, schemed to get their representatives onto World Health Organisation (WHO) specialist panels where they could push a particular commercial agenda for a particular drug regime or against a specific regulation. The possibilities for corporate enrichment for very little investment were (and still are) vast.

But the financial world’s influence wielders – successors to those who caused the 1929 crash and then benefitted from it – had a broader vision, not unlike that of the founders of the South Sea Trading Company. They aimed to make debt and debt trading so commonplace that everyone on the planet would eventually be caught up in it. That meant developing and imposing strategies that gave ordinary people no choices.

They were worried by the powerful post-WWII trend where governments and public bodies built and provided housing for their populations. Many still view the 1940s to 1970s as a golden era in public housing and services. Public housing investment and the benefits of having populations decently housed at a reasonable cost to each household contributed directly and indirectly to the post-war boom. In the 1950s, the WHO defined “housing poverty” as a situation in which a household was spending more than 10% of its income on housing provision (later rising to 20%). In London, England, where I am writing this article sixty years later, that looks like a fairy tale aspiration. Households here frequently pay over 60% of their income on housing provision.

In 1976, Canada hosted Habitat I, the UN’s first Human Settlements conference, recognizing the importance of the world’s growing urbanization. It showcased some of the world’s most successful housing practices with no single model dominating. Publicly provided, co-operative, co-owned, private rental, co-housing, self-built, community-built housing models and more were presented, studied and compared. Whole new academic disciplines emerged. The United Nations set up UN Habitat, the Nairobi-based UN Centre for Human Settlements (UNCHS). Governments committed to massively ambitious (and possibly unachievable) programmes like the Hundred Thousand Houses programme of Sri Lanka, launched by then Housing Minister Ranasinghe Premadasa in the late 1970s, subsequently expanded to the Million Houses Programme when he became President in the 1980s. McGill University established its Minimum Cost Housing Group focusing on developing countries. Best practices from previous decades were shared and developed further. Significant progress seemed possible. And despite problems, including potential corruption, public provision appeared to be an efficient way of providing housing on a massive scale.

This put public bodies at odds with the followers of Ayn Rand, Friedrich Hayek and Milton Friedman, whose long-term aim was to force the world population into debt. Limiting the production of housing – like gold, diamonds or oil – could persuade people that housing was something to strive for. The term “aspiration” was employed. Housing supply was limited, bolstering concepts of scarcity, rarity value and ever-rising prices. Having popularized the idea of shrinking the state, they expressed implacable opposition to state provision of anything (except the military), especially housing. Making private housing desirable by limiting its availability clashed with governments’ enthusiastic support for public housebuilding. They also used softer approaches to transform expectations in developing countries. For example, The East Africa Building Society (a savings and loans bank) set up in the late 1950s to promote individual home ownership, had window displays of happy African families with 2.4 children in front of suburban detached houses with a car in the driveway – the East African variant of the American dream. Subsidies to private provision and ownership had certainly helped boost private housebuilding, but not on the scale the monetarists wanted.

Against this, the UN Centre for Human Settlements was training and advising governments and communities on non-private provision (as well as best practices and technical assistance on regulating private housing). These programmes increased public debt in the short term without imposing it directly on the residents of such housing. It took that unholiest of alliances, Reagan and Thatcher, not acting individually but together as representatives of “big debt,” to achieve that change.

In 1980, Margaret Thatcher introduced legislation in Britain forcing local authorities to sell their public housing at a loss (described as a discount), and preventing them from building more to make up the resulting shortfall (despite initial claims that any income generated would be used to build new housing). Almost without exception, people who exercised their right to buy had to incur debt in the form of private mortgages.

Some final pieces of the international jigsaw were ready to be put in place in 1986. Ronald Reagan, publicly attacking the profligacy of the United Nations and frequently citing corruption or maladministration while suggesting the presence of reds under UN beds, cut US funding to the UN and many UN agencies, saying it would only be restored when the US was satisfied. These cuts came on the back of earlier cuts. As the US was the largest funder (at around 25%), this was significant. The UNCHS slashed programmes that would not have garnered the approval of Reagan and Thatcher. Seminars, courses, training schemes intended to help governments develop the best and most appropriate practices to meet their needs were suddenly suspended for lack of funding. Salvation, when it arrived, came from a perhaps unexpected source.

The organization that stepped forward was the World Bank, ready to restore some of the funding that had been cut. All it wanted in return were a few policy tweaks. Reagan and Thatcher appointees were in place to call the shots. The UNCHS Habitat was to promote private housing provision, to be paid for through household debt, mortgages and loans, preferably through banks, building societies and savings and loans banks. The model was established: housing privately built (possibly with a little public seed funding), privately purchased through private financing from private banks or other institutions. To make the change more palatable, the concept of “affordability” was introduced. This had nothing to do with ensuring whether housing was within the financial means of a household, as the old concept of “social rents” had done. It was simply a mathematical formula that determined that housing was “affordable” if it was cheaper than prevailing market rents for the same area and housing type (often by 20%). In discussions about what this would mean for the poorest in the world, it was conceded that the poorest tenth percentile of the population would be excluded. In many poor countries, that is the majority of the population. In other words, the poor, who were unable to pay mortgages, were ignored. The policy simply didn’t apply to them. Governments around the world started to fall in line.

Keen to be viewed as being on message, like many other academic bodies concerned about their funding in the new world order (in this case, Brian Mulroney’s world order), McGill University’s Minimum Cost Housing Group rebranded itself as the Affordable Housing Group, shifting emphasis away from community and public provision-based approaches towards debt-based models. And for good measure, it developed some concrete housing that could be manufactured in Canada and sold to Mexico, obviously via a private mortgage-based housing system. A complete turnabout.

So now, the poor be damned! There was now one single model, based on individual indebtedness, promoted around the world as UN policy and supported by the World Bank, the IMF and multiple governments.

Around this time, Ronald Reagan, through his Vice President and deregulation czar, one George (H.W.) Bush, deregulated US savings and loans banks in 1988. Fortunes were made overnight by their directors or owners. Fortunes were lost by banks and homebuyers. The resultant financial disaster led to a crash in the bodies providing private financing for private housing. It was effectively a dress rehearsal for the crash of 2008. Logic should have decreed that this would derail the programme, but enough people were now in key positions to defend it, so it continued. Soon afterwards, then President George (H.W.) Bush enacted a rescue programme that he promised Congress would cost the US 168 billion dollars. A decade later, Stanford University’s analysis revealed that it actually cost the US about 1.4 trillion dollars. After a short period during which a few minor prosecutions occurred very publicly (the Bush family members who were involved were spared), many of the crashed savings and loans banks were given government funding and returned to the people who had busted them, leaving them to continue doing what they had been doing before. The ripples settled, and it was back to home-financing business as usual until 2008.

In Japan, following a similar property crash in the 1980s, the public never returned to the reckless and extravagant home-buying practices promoted in its boom, and Japanese consumers remain reluctant to take on debt. In Spain, a similar crash left 3 million families without homes, while 3 million non-habitable homes (homes not completed, below habitable standards, with no services or access, or abandoned during construction) stood empty. It is still far from recovering. In China, entire speculative cities stood empty.

By 2007, US debt that had been transformed and resold in packages (“collateralized debt obligations” or CDOs), with slivers of secure debt mixed with poor risk debt, was being marketed as “sub-prime” mortgages. Home ownership by private debt as the sole model had been heavily promoted. People who could never repay had been granted mortgages. House prices had been driven up relentlessly, and people were panicked into buying because if they didn’t do it then, they would miss the boat. The system could not be sustained. It crashed, taking with it some of the biggest banking institutions in the US and around the world.

Somehow, partly as a result of its then stricter banking regulations, Canada avoided the worst of the 2008 crash. US property prices tumbled. In Canada they dipped before rocketing more recently to astonishing, unprecedented levels. People ended up panic-buying into rising markets, convinced that if they didn’t get on the property ladder immediately, they would be excluded for ever. This fear has driven price increases in major Canadian cities to among the highest in the world. Bloomberg has frequently warned they are unsustainable.

As Canadian housing prices start to slide, pundits for the debt system are being recruited to explain that the dip is a blip. Like paid climate-change deniers, they interpret this as a local micro-climate. But Canada, like China, subject to the same global principles, may be about to rediscover that no alliance, however UNholy, can override gravity. What goes up – overheated house prices – eventually comes down in a torrential market collapse.